One of the top challenges B2B marketers face in setting their budget is attributing marketing to revenue results.1

While it should come as no surprise that executives hold their marketing departments accountable to delivering bottom line results, many marketing leaders struggle to make the case for their budget, let alone defining a profitable marketing metric.

To overcome this challenge, marketers should point their executives toward customer acquisition and customer value. Calculating customer lifetime value is the first step in making a long-term business case for your annual marketing budget and plan.

What is customer lifetime value (LTV) and how does it change how I look at my marketing program’s ROI?

The lifetime value of a customer is the total value, or monetary worth, of a customer’s business over the lifetime of their relationship with your company.

While a return on marketing investment (ROMI) can be calculated on an initial customer purchase, the customer lifetime value is calculated over the life of the customer and places value on all purchases made including the initial sale. The graphic below shows how ROMI is calculated for a one time investment.

Relationship between Marketing Investment, Revenue, Gross Margin & Return

A ROI that aligns with the customer lifetime value model takes into account all investments made to acquire and nurture customers over their lifetime and all incremental customer value generated as a result of those investments.

Here’s an example of how using the customer lifetime value model shows the true profitability of a marketing campaign compared to a monthly ROI analysis.

Lets say that it cost a manufacturing company $10,000 to acquire five new customer last month through its paid media channel. Those five customer purchased enough services to bring in $9,000 in profit. An analysis within a one month window of this company’s paid media ROI would should show this marketing channel in the red.

Now, let’s examine this same scenario within the customer lifetime value (LTV) model.

The company has calculated the lifetime value of a particular customer segment they just acquired to be $7,500 per customer from additional investments made in cross-selling and upselling over the next 5 years. Instead of a $1,000 loss, the lifetime value derives a $37,500 profit helping stakeholders recognize the positive return.

Calculating Customer Lifetime Value (CLV or LTV)

Calculating customer lifetime value requires combining the expertise of a variety of professionals inside your company, including accounting, sales, analytics, and IT. It also requires a common understanding of how value will be calculated. For example, “Do we calculate revenue only, or do we assign a value to other customer actions, like advocacy as well? After all, this is worth something to our business, but how do we assign a dollar amount?”

Lifetime value is especially tricky for B2B manufacturing companies to calculate due to the complexity of customer interactions and distributor relationships.

The most important guiding principle when calculating LTV is to make sure that only the stream of revenue and profit generated by the specific investment over time being measured is included in the calculation, not any additional investment.

Once the LTV is defined, celebrate the victory and then catch your breath. You’ll now want to get to work on your allowable acquisition cost. This will help you to define how much you can spend to acquire each new customer and be profitable.

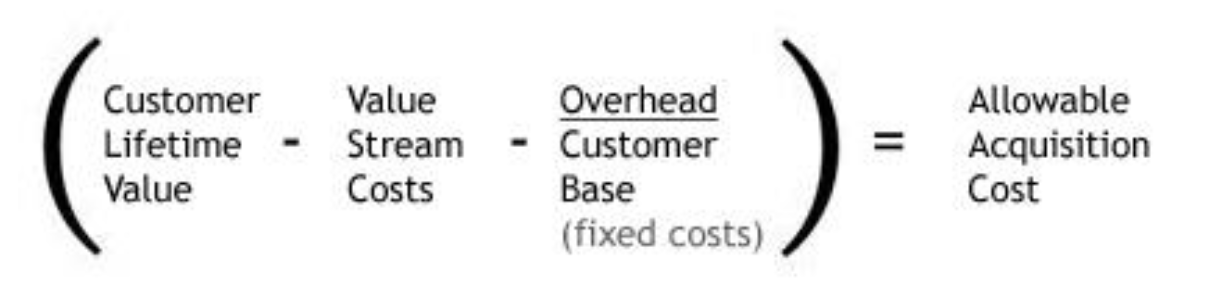

What is Allowable Acquisition Cost (AAC)?

The allowable acquisition cost of a customer is the amount of money a business is willing to pay to acquire a new customer. The higher the lifetime value of a customer, the more a business can justify spending to attract and retain customers.

Allowable Acquisition Cost Calculation2

Who should calculate your allowable acquisition cost (AAC) and customer lifetime value (LTV)?

Your company’s CFO is typically the most qualified individual to calculate customer lifetime value and customer acquisition cost. It is essential to seek out this individual and their help. While the formula for allowable acquisition cost may appear simple, the values that go into each part of the formula are open for debate.

For example, one company may calculate its value stream costs with the facilities cost but not the maintenance cost. Value stream costs is a consolidated metric that includes all costs, direct and indirect, that go into bringing a product or service to market, including, but not limited to labor, machine, materials, support services and facilities.

The allowable acquisition cost formula above is just one of many ways that companies choose to calculate an acquisition cost that achieves profitability.

Lifetime value, as touched on above, will undoubtedly be the most challenging to calculate. Some businesses will incorrectly calculate the lifetime value of a customer based on revenue, while others choose to calculate it based on profit margin.

In some cases, organizations lack the data points to fully calculate the lifetime value.

If you do not have the expertise in house to calculate this value, it is worth hiring an external analyst to help aggregate the appropriate data and get to an actionable AAC.

With your allowable acquisition cost and your acquisition goal defined, you are now ready to calculate your annual marketing budget. As long as your organization doesn’t have capacity limits, you can scale your growth until you reach your allowable acquisition cost. Allowable acquisition cost is a critical metric you will need to make the business case for your marketing budget. It will allow you to know exactly how much you can spend in order to grow profitably and reach new heights.

1Forrester Research, Inc. “Q3 2013 North American B2B Marketing Budget Online Survey.

2Josh Kaufman, “The Personal MBA, 2nd Edition.”